Aside from the stressors of college itself, paying off student loan debt is another impossibly difficult task, even if you live off a generous income. It’s all the more difficult when you’re barely getting by and hardly make enough to even cover your bills.

And in this regard, college graduates are the most burdened of the lot.

Recent graduates carry an average student loan debt of $37,172, with a 6.8% interest rate. And if you were unfortunate enough to get an adjustable rate, by the time you get decent paying job, the interest rate will have spiked its way up too.

That’s not to mention you still have to pay for other living expenses like groceries and car payments. Paying even the minimum amount, which you’re advised to, can be very challenging.

Having a higher salary would be a great boost, but if you can’t order money to your whim like that, here are some tips:

1. Change your mindset and get organized

First things first, you need to organize all your debts to get a clear picture of how much you owe. A great part of this is going in with a champion sort of attitude. If you approach it feeling beaten and defeated already, you won’t make much progress.

You should understand that despite money being the only way to pay off all that debt, it’s not the most important thing to focus on. You could suddenly get a six figure salary and pay off all your debt, only to land right in again.

Besides, there are plenty of six-figure-earning people out there drowning in more debt than you could imagine. One of the most important aspects of being able to pay off virtually any amount of debt is money management skills.

Set some goals for yourself and reward yourself when you achieve them to feel motivated to go on. Envision what a debt-free life will be and set aside money to fulfill those goals once you manage to find your way out of the cesspool of debt.

Once your head is in the right place, get down to the numbers. How much do you owe, who do you owe and what’s the interest rates each charges you?

2. Break up your big goal into smaller chunks

After your goals have been set, break them into more divisible chunks. This way, they are much easier to pay off without turning you inside out in hunger or in cold for the lack of a roof to sleep under.

While you’re at it though, remember that the last thing you want to do is pay the minimum amount of cash that your loan allows.

For instance, let’s say you have a $45,000 student loan debt, but you only earn $35,000 a year. Obviously, you’re not going to be able to pay that off in two years, even less so in just one, considering all the bills you have to pay and what not.

You’ll have to set realistic goals.

You could pay down around $10,000 a year by putting aside $833+ every month and being extremely careful about your spending. That’s more manageable and easy to track. Once you’re able to achieve this goal, feel free to reward yourself and begin focusing on the next one.

While that might sound impossible, the reality is if you really want to get rid of your student loans, you’re going to have to make sacrifices and get smart about your money.

Here’s a great video that breaks down how to set financial goals that you’ll actually stick to:

3. Choose a debt repayment strategy

If you have a small budget to work with, you’ll have to be strategic about how much in expenses you’re willing to sacrifice towards debt. This is one of the reasons why debt repayment strategies exist.

Choose one that makes the most sense for your budget and will help you achieve the best results in the shortest amount of time.

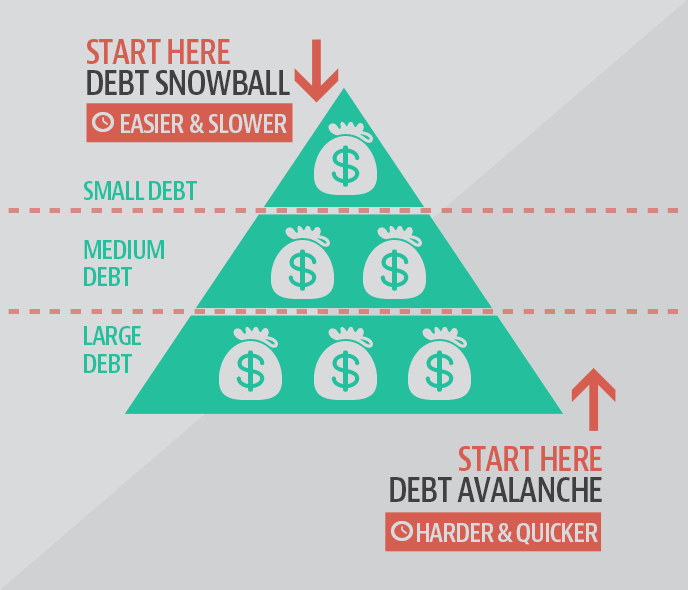

If you want to get rid of the debt faster, the general way of approaching it is pouring more cash into paying them off. The most common ways to do so are the snowball method and the avalanche method.

The snowball method involves starting off small and picking up momentum along the way as you go. You start by focusing on the smallest debt first. Add more money into the repayment of the smaller loan, all the while contributing to the other loans, too.

Once you’re able to pay off that, focus the money, that should at this point be extra, into the next smallest balance. Repeat the process until only the largest debt is paid and wring it out the quickest you can.

The snowball method is one of the most favored since it gives great motivation. Once you pay off one of the smaller loans, it gives you a sense of accomplishment and you can see the progress you’re making.

The avalanche method works similar, only this time, it’s focused on the debt that has the highest interest rate. Basically, concentrate more money on paying off the highest-interest debt and continue until only the lower-tier ones are left.

This method is most suitable for people with lower incomes.

Every dollar that’s sacrificed and put towards debt repayment is super important and will help you go further with this strategy. Besides, if you’re looking to save the greatest amount of cash in the long run, the avalanche method should work just as great for you.

Not sure which method is right for you? This handy calculator will help you decide whether the avalanche or snowball method is better for you.

4. Cut down on miscellaneous expenses

The point of a solid budget is to help you know where most of your cash is going. It should help you keep track of the high-cost and low-cost expenses, especially on a low income. Once you have it down, start getting rid of any expenses you can reduce or cut off completely.

One of the biggest money drains is eating out. Try to cut off your budget and teach yourself to cook instead. Sure, it will be horrible if you’ve never cooked before, but you’ve got to start from somewhere.

Maybe you can even take a short break from the gym for some time during the year and save money on clothes by shopping during sales and using coupons. You can even cut off cable and just pay for a Netflix + Hulu subscription instead.

If you can get some hands-on experience with cars and learn to service it by yourself, you could save thousands a year.

Lowering your monthly expenses and embracing the value of being frugal will create extra money that you can pour into paying off your debt. Once you’re done with the repayment process, you can consider going back to the old lifestyle.

5. Earn more money, somehow.

Even though the options above will help you pay off your debt faster, focusing on getting more income will help even more. Nobody denies that it’s possible to pay off a ton of debt even if you’re living on low income. However, there are limits as to how much you can pay off each month.

Earning more money will make your progress through the process even quicker.

There are a number of ways you can generate more revenue: ask for a raise, get a new job or pick up a side hustle. The latter option is the easiest and quickest to act on quickly.

If you have any skills, you can use them to earn some extra cash around your full-time job. Otherwise, there are a lot of other side hustles that guarantee flexible hours like photography, assistant work, driving an Uber and walking dogs.

Once you’re able to get a job, the secret is to avoid inflating your lifestyle with more gunk than necessary. Instead, focus the extra money towards paying off your student loans.

You can pay off student loans on a low income

Contrary to popular belief, you don’t have to be rich in order to repay your student loans. Sure, it’s more difficult to pay back Navient and Great Lakes when you’re living paycheck to paycheck. But difficult doesn’t mean impossible.

Use the tips above, be patient and over time, you’ll be free of college debt for good!