You’ve had enough of stretching every last dime between meager paychecks. You’ve had enough of crouching under your desk whenever you hear whispers about layoffs.

And, maybe you’ve had enough rent increases and noisy neighbors in your cracker-box apartment.

So, you look at rising home values. You hear about investors who started with nothing and now buy and sell properties (or exotic options on properties) like they’re owning their little cousins at a game of Monopoly. You hear about people not much older than you enjoying income from multiple rental homes. You hear it’s easy if you do it right.

Yeah. “Easy.” Maybe not so much.

Still . . .

The Constant Lure

Real estate investment is a constant lure because it works. Investing in real estate can create personal wealth - when it's successful.

But it isn't always successful. And oftentimes when it fails, the reason is this:

New players in the real estate game don't realize it's more than an investment. It's a business. Success in business demands preparation, and always entails some risk.

Homeowner or Deal-Maker?

Anyone who owns a home is already a real estate investor, actually.

We Americans take homeownership quite seriously. "Homeowner" is almost synonymous with "Responsible Grown-Up." For generations we've encouraged home ownership as the solution to every social problem from crime to poverty to poor child-rearing.

Homeowners are the backbone of America, most would have you know. We tend to look after them in certain ways - like allowing them to deduct the interest paid on mortgages from their income tax. It’s because they are investors in . . . AMERICA!

So, after thinking it over a bit, perhaps simply owning a home you might one day sell at a profit or rent out to a tenant might be enough real estate investing for you.

But there are many other ways to play the real estate game and make money, and not all of them involve actually taking residence in or even ownership of a house.

At this point you have to ask yourself which you value more: Quiet, comfy nights in your own home which is gaining value and which you might one day rent out, or cash from investment plays based on America's love affair with real estate?

The answer to this single question will determine the rest of your journey.

Stay or Play?

The advantages of ownership of a residential or investment property include:

- Tax deduction of mortgage interest

- Ability to borrow against the property, and the ability to deduct the interest on that loan as well.

- Insurability against loss due to theft, damage, or disaster

Oh, and another good thing about owning a home is that you can live in it. Quite literally living inside your investment has a great appeal to some.

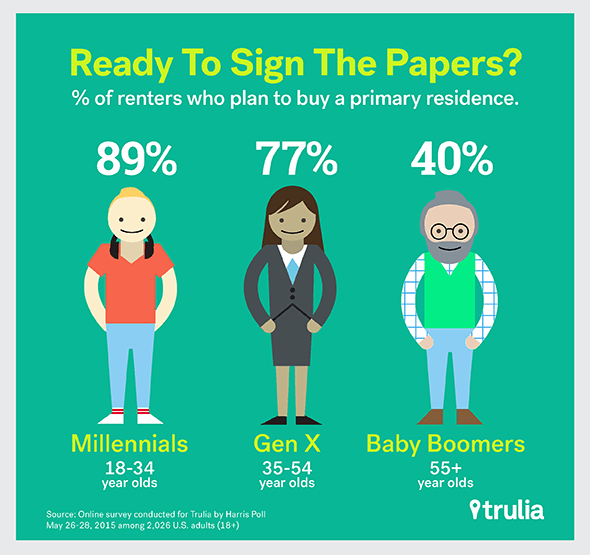

A great trend we're seeing is more millennials looking into purchasing versus renting. Trulia found that millennials (18-34 year olds) are the main age group ready to buy.

Of these advantages, precisely none apply to the gains you'd realize as a trader of lease/buy options, or a wholesaler of home contracts, or an investor in a real estate investment trust (REIT), which is basically a fund that invests in real estate on your behalf.

Of course, there are drawbacks to owning a home:

- Upkeep: Houses and their contents wear out and need maintenance.

- Illiquidity: You can log into your brokerage's website and sell out your position in a REIT in seconds. You're not going to do that with a home. You might find you're stuck with it - at least for a while.

- Property tax: In some areas this can be a real killer.

- Rental marketing and tenant relations: Finding and keeping good tenants can be a chore. Dealing with bad tenants can make you believe perhaps you weren't meant for this cold, cruel world after all.

Your choice will depend on where you are in life when you start, and where you want to be in the few years. Staying or playing can each be equally-valid ways to do the real estate thing.

Let's say for the time being you choose to actually take ownership of a property, either as your main residence or as a rental unit.

Homework on Homes

Before you get started, you have some homework.

Research, research, research: You need to research everything about owning and investing in real estate. You need to ingest before you invest.

Here are are a few topics for further investigation:

- Is the market going up or going down? People usually get the real estate bug just as the market is peaking. When you start hearing mortgage tips from the guy selling you a Slurpee at 7/11, it's a good bet the market is about to tank - just like it did back in 2006. Remember: the goal is to buy low and sell high. Many homes purchased at the peak of the real estate boom of the 00's are still underwater.

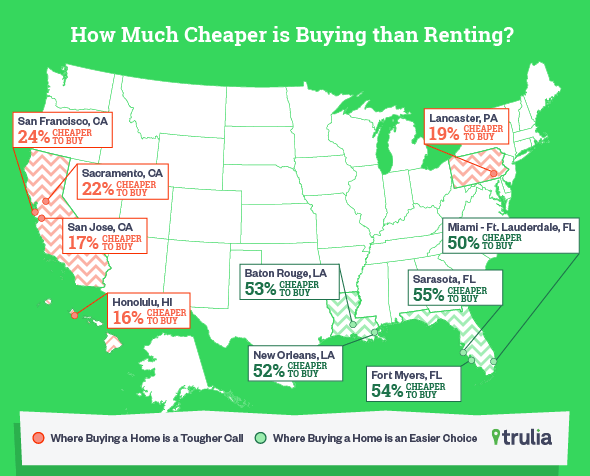

- Is it cheaper to buy or rent in your area? There are owners' markets and renters' markets. If you're buying a house specifically as a rental, you might find rent income won't cover your principal, interest, taxes, and insurance (PITI). Homes in these markets can still be profitable at resale time, but you'll need to budget around the monthly difference between inflow versus outflow. Plus, most savvy investors advise a 5% margin above PITI for upkeep and unforeseen expenses.

- How’s life for landlords in your town? Landlord laws vary. In some states it's almost impossible to evict a renter no matter how destructive or delinquent. Then there's Colorado, which insists landlords provide renters three whole days notice before kicking them out on the street.

- What's your time horizon? As stated before, market dips can last years. Most experienced investors advise a minimum timeline of seven years to ensure you'll make money on the resale of a house. Could you hold a property that long, if necessary?

- What about your personal credit rating? Your credit will determine which mortgage programs are available to you. The higher your FICO score, the lower your interest rate, and the better the terms. It's worth gathering your credit reports from the three major bureaus and addressing any issues on them sooner rather than later. The further those bad marks fade into the past, the less they affect your current score.

In short: approach real estate investing as you would a new career.

What to Buy

So you've done the homework. You know state of the market. You know your local laws for landlords like you know your own mother’s face. You've cleaned up your credit reports.

Now, what to buy?

Your choices will likely come down to a single-family home or a condo.

There’s an old saying about the advantages of investing in real estate. It goes: “They’re not making any more of it.” That’s a reference to how the earth is approximately 25,000 miles around, with about two thirds of that covered by water. “They" are not making more land to be sold as real estate, so of course it’s a great investment. Scarcity, right?

But see, when it comes to condos, “they" still are making plenty of “it.” Apartments are converted from rentals to condos all the time. New condo and patio-home buildings are going up all the time. Condo towers sprout from small patches of that supposedly-scarce real estate, multiplying available space as they reach to the heavens.

When it comes to condos, they are still making more of it, and almost no one seems to want the old stuff.

Condos have some serious drawbacks as real estate investments. First, there’s the false scarcity issue: New condos dilute the value of existing stock. Then there are HOA and management fees, which can be considerable. These fees - unlike mortgage interest - are not tax-deductible.

Finally, condos might not have all the maintenance requirements of single-family homes, but the HOA often will levy “special assessments” to fix things like parking areas, shared plumbing, and climate control. These assessments can run into thousands per unit and are not tax-deductible. In many cases, you’ll find you can’t even pass them on to a renter. You’re not likely to tell your renter she owes you another $3000 this month for repairs to a shared roof.

For renters, a condo can be a great experience. For owners, they can be financial disasters in the long run. Condo owners can find over time their “investment” doesn’t even meet that most basic criteria applied to an investment: the value of their home didn’t even keep up with inflation.

This isn't to say you can’t make money buying, renting, and selling condos. It happens all the time in some markets. It’s just usually not the way to bet.

If you’re in this to make money over the long haul, chances are a single-family home is the way to go.

Where to Buy

Andrew Tobias wrote a great little book called The Only Investment Guide You'll Ever Need. In the chapter on real estate, he offers some very simple advice: Don’t buy a rental house in a neighborhood where people jog.

See joggers? Buy elsewhere.

For more than thirty years, The Only Investment Guide You’ll Ever Need has been a favorite finance guide, earning the allegiance of more than a million readers across the United States. Now even more indispensable, this completely revised and updated edition will show readers how to use money to their best advantage in the wake of epochal change on Wall Street, no matter how much or how little they may have.

Tobias explains:

- How virtually any reader can save more than $1,000 a year

- How and when to invest in stocks

- The “safest investment in the world”

The logic is simple: If people have the leisure time and self-focus necessary to jog, they likely have good jobs. If they have good jobs, they likely won’t be renters, or at least won’t be renters for very long. Turnovers in a rental house can be expensive. You want long-term renters.

Tobias advises buying a sturdy house in the sort of working-class neighborhood inhabited by the sort of people who find it very hard to save up enough for a down payment. These people often rent for years on-end.

When shopping for an investment property, you need to be sensitive to the needs of your potential renters. Convenience to grocery stores, mass transit, and schools usually top the list of desired features.

You’re not renting to affluent fashion victims: You’re renting to survivors.

The Fixer-Upper Fallacy

Sweat equity has a great, noble ring to it: Sweat. Yeah, you paid for part of that house with the sweat of your own brow - just like a frontier homesteader.

It works out - sometimes.

Pros & Cons Of Investing In A Fixer-Uppers

PROS

- Less Competition

- Forced Appreciation

- Unique Financing Options

CONS

- Hidden Expenses

- Stress

- Potentially More Out-of-Pocket Costs

But if you aren’t quite Herbert Handyman, and if your tools consist entirely of a single IKEA screwdriver set, you’re likely going to need to hire contractors for your renovation project. Contractors get expensive, very fast.

Some fixer-uppers can be rented or resold with only a good cleaning, new paint, new flooring, and a few repairs. A variety of investor called a fixer-flipper looks for these quick-fix candidates. This market is competitive. The country seems filled with fixer-flippers. Their rivalry tends to drive up the prices of fixer-upper homes as they fight to see which new owner gets to remove the cat-urine-soaked green shag carpeting.

Unless you have time, tools, and skills, leave the fixers to the fixer-flipper cult. Look for a house that needs little to nothing to be livable and marketable.

Financing: “Creative” Does Not Equal “Crazy"

With the implosion of the sub-prime mortgage market in 2008, it became very hard for the cash-strapped investor to get financed. The zero- or almost-zero-down mortgages once offered by big lenders disappeared. Now, they are gradually returning. Bank of America, for one, is advertising zero-down financing for very well qualified borrowers with close to perfect credit.

Some zero-down programs never stopped. The USDA has a zero-down program. Despite the name, there are some urbanized areas where they’ll finance a home. The VA has long offered zero-down financing to veterans of the armed services and their family members. Navy Federal Credit Union is another zero-down option for former service people and their relatives. Most of these programs build a small loan servicing surcharge into the interest rate to compensate for the lack of a down payment.

Many state and local governments offer zero-down programs for first-time buyers. Sometimes, they require the home be used as the buyer’s primary residence - at least for a while. Also, the programs might only apply to certain (usually blighted) parts of town.

Most of these programs will allow the inclusion of closing costs in the loan balance, making for a true zero-down experience.

If you don’t have a 20% down payment, most non-VA, non-USDA loans will require private mortgage insurance (PMI). PMI is bad news in that it isn’t tax-deductible, and buys the homeowner basically squat. However, once equity in the home increases beyond 20%, most lenders will allow the removal of PMI after the homeowner pays for an updated appraisal.

If you're considering getting into real estate without much of a down payment, don’t overlook the chance to call upon the help of parents and relatives. Sometimes, the best mortgage lender is the First Bank of Grandma.

All of these count as creative approaches to financing your home. But there’s creative, then there’s crazy.

Explore your options for financing your first real estate investment. There are plenty of ways to get homes for zero money down.

Something Closer to Crazy

There are private lenders who will finance all or almost all of a home purchase, usually at higher interest rates, and for shorter terms. They call these "hard-money" lenders. These lenders frequently offer “no-doc” loans, meaning they don’t require tax returns or proof of employment.

Hard-money lenders can be a godsend if you know what you’re doing. If you are willing to make a bet that the home you’re eyeing will gain 30% in only 18 months, hard-money can get into it quickly and easily, then let you walk away with a handsome profit after you’ve resold it and paid back the private lender in full. That is, if your bet is right.

It’s really less like investing, and more like gambling.

Summary

It is indeed possible to make money investing in real estate, and the returns can be quite handsome, given a long enough timeline. Taking investing seriously as a business decision is the first step toward a successful outcome.

But there’s another important factor to consider: You.

Being house-rich and cash-poor isn’t usually a recipe for joy. There have been so many plans that would have worked perfectly had it not been for that pesky, human need to feel good about life. The ultimate purpose of any investment strategy is your own personal satisfaction. Keeping this single thought in mind will serve as a better guide than a thousand articles like this one. You should live and invest to be happy.

And really, that should be enough.