Getting into debt can be pretty easy, especially when you’re just getting the hang of your finances. But while it is easy to take out loans, max out credit cards, and finance everything from computers to cars, making payments to get out of debt isn’t so quick and simple. Debt consolidation can help.

For anyone struggling to get out of debt, debt consolidation may be able to help. This guide can help you decide if you’re one of the people that may benefit from consolidating their debt.

About Debt Consolidation

Before we get into whether or not consolidating your debt is the right choice for you, we need to address what debt consolidation is. For many people in debt, they have small chunks of money that they owe scattered throughout different loans, credit cards, and financing agreements. Each of these debts has a different payment date, interest rate, and amount due.

With debt consolidation, you agree to one loan that covers all the loans that you currently owe. With the money you receive from your consolidation loans, you completely pay off the original debts. Then, you just have to make one monthly payment on the larger loan.

Debt consolidation is not designed to lower the amount of money that you owe and it won’t ruin your credit score. Instead, all it does is put your payments in one place with one monthly due date and a set interest rate.

While debt consolidation sounds like a good idea for everyone, it does have some drawbacks. Here are the pros and cons of debt consolidation.

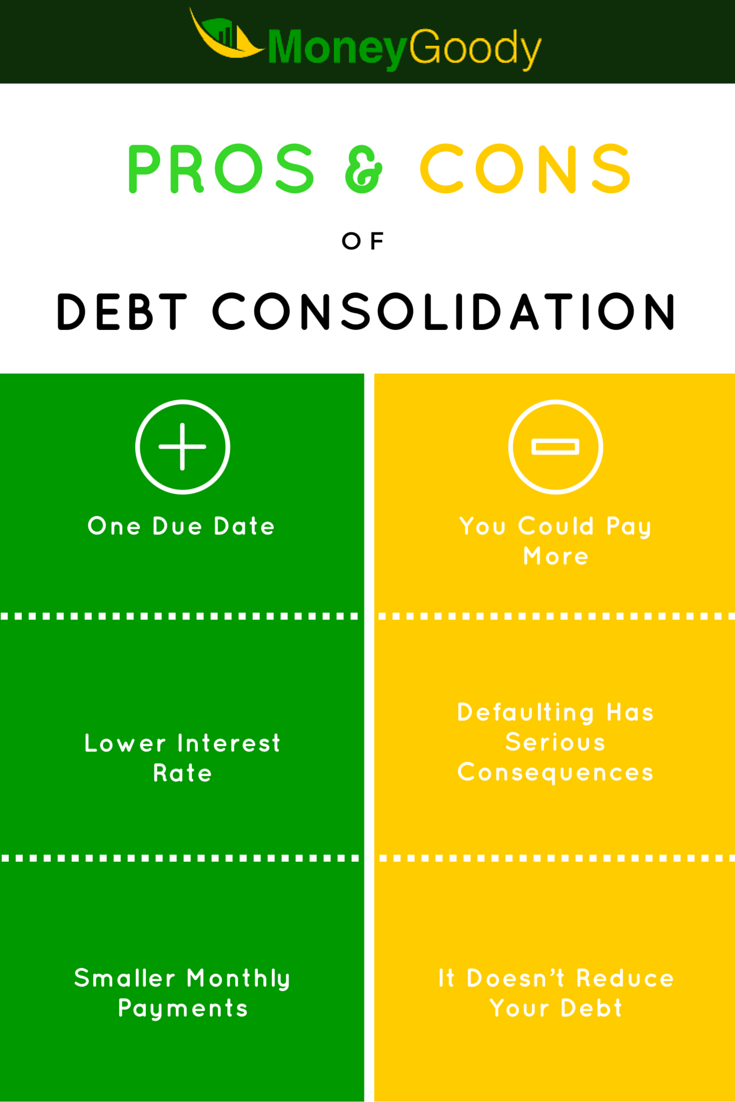

Debt Consolidation Pros

To start out on a positive note, we’ll take a look at some of the great things that debt consolidation can provide.

1. One Due Date

When you’re trying to make payments in a million different places, it’s easy to fall behind somewhere. Time gets past you and suddenly you’re remembering that you had a payment due a few days ago.

Forgetting to make payments on all of your debts can cause late fees and additional interest to accumulate, meaning every time you miss a payment you’re getting further and further into debt.

But when you only have one due date to worry about, it’s a lot harder to get stuck behind. You don’t need to worry about making a new payment a few times a week. Instead, you just need to mark the date on your calendar and continue living your life!

2. Lower Interest Rates

The loan you receive from debt consolidation usually will have a relatively low interest rate. In some cases, the consolidated loan will take the average of the interest rates all of your outstanding debt and use that as your new rate. This can allow you to pay less in interest than you otherwise would have.

You can also consider that with interest accumulating on only one loan, you could save hundreds or thousands overall depending on the amount that you owe. Saving this money can help you build a savings while in debt or allow you to get out of debt more quickly.

3. Smaller Payment Amounts

With your original debts, each had their own life span. One’s final due date might have been just around the corner, meaning you needed to make high payments every month to pay the loan off in time.

But with debt consolidation, you’re giving yourself time to pay off the loans. This allows the loan to be spread out over a longer period of time, so you are able to make smaller payments each month. Because the interest rate is likely going to be lower, you’ll also be paying less interest each month.

Debt Consolidation Cons

While it may seem like a great thing to pay smaller amounts each month with lower interest rates, not everything about debt consolidation is positive. Here are a few of the drawbacks that come with consolidating your debt.

1. You Could Pay More

Even when you’re paying less money each month with smaller amounts of interest, you could still end up paying more in the long run. Remember, debt consolidation does not forgive you of any of your debt. Instead, you’re just putting it into one place.

This means that when you’re paying less on the same amount of debt, you’ll pay the debt over a longer period of time. This allows interest to accumulate for longer, so even if the rate is lower, it has more time to build. Be sure to do your research to see if you’re getting a good deal.

2. Defaulting Has Serious Consequences

One of the most popular forms of debt consolidation is through a home equity loan. With a home equity loan, you are essentially using your house as collateral if you have to default on the consolidation loan.

Falling behind on a secured debt allows your creditors to take control of your possessions. If that is your house or a car, they can sell that piece of property in order to cover your debts. It is very important to meet the demands of your new loan if there is something serious at stake, such as your house.

3. It Doesn’t Reduce Your Debt

While debt consolidation can help make your debt more manageable, it doesn’t relieve you of anything that you owe. It shouldn’t be viewed as a quick and easy way to get out of debt and shouldn’t be confused with filing for bankruptcy or going through a debt settlement process.

If you are very deeply in debt, consolidation may not be the right option for you. In order to get yourself out of debt, you may need to make some lifestyle changes. Getting a second job, shopping frivolously, and avoiding any excess spending are sometimes necessary to begin digging yourself out of your hole.

Consolidating Student Loans

One of the first experiences most young adults have with debt consolidation is student loans. For some schools, your student loans may have been taken out per semester, or even with different lenders.

As a result, you probably have multiple loans with different rates, amounts and due dates. It’s a mess.

If you’re in a position where your school loan payments are too much, consolidating them can help you save some money. The government actually has a program in place to consolidate your federal student loans, called a Direct Consolidation Loan. A direct consolidation loan is:

A federal loan made by the U.S. Department of Education that allows you to combine one or more federal student loans into one new loan. As a result of consolidation, you will have to make only one payment each month on your federal loans, and the amount of time you have to repay your loan will be extended.

You can apply for a direct consolidation loan through studentloans.gov.

Another option for consolidating student loans is through private lenders. There have been a few popping up recently, and one of the most popular is SoFi. The benefit of SoFi or similar companies is that you can consolidate both federal and private student loans.

Since private student loans tend to have much higher interest rates than federal, SoFi is a great solution to get your private loans lowered to a more reasonable interest rate. And just like direct consolidation loans, the length of the loan is stretched out so your monthly payments are lower and you pay less interest over time.

You are the only one that can decide if debt consolidation is right for you. Consider these lists of pros and cons, assess your debt, and make a decision if you believe it will help you climb out of debt.